Shipments of both tablets and notebooks will continue to decline in 2017, according to TrendForce.

Notebooks

Shipments of both tablets and notebooks will continue to decline in 2017, according to TrendForce.

Notebooks

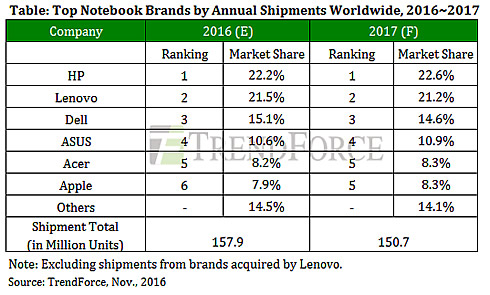

Global notebook shipments for 2016 is estimated to decline by 4% compared with the prior year to around 157.9 million units, reports research firm TrendForce. Notebook sales this year have been constrained by rising prices and supply shortages in the component markets. Global notebook shipments for 2017 are projected to total 150.7 million units, representing an annual decline of 4.5%. Notebook shipments will continue to fall next year as the LCD panel market experiences a structural supply shortage.

"Global notebook shipments have been on a slide for two consecutive years starting in 2015," said TrendForce notebook analyst Anita Wang. "The structural supply shortage in the LCD panel market will contribute to further decline in notebook shipments during 2017.” Wang pointed out that shipments of HD resolution (1366 x 768), Twisted Nematic (TN) panels for mainstream-size notebook displays will decrease by 10% between 2016 and 2017.

"Branded notebook vendors will release more new models featuring FHD resolution (1920 x 1080) display," Wang added. "However, selling more FHD models to offset the lack of supply for HD models may not be a viable strategy. First, FHD LCD panels cost much higher than HD counterparts. Moreover, notebooks that are equipped with 8GB of RAM and a FHD display belong to the high-end premium category, according to Microsoft’s current formula for Windows license fee. Higher hardware specifications will lead to a significant rise in that notebook’s OS license fee, so branded vendors will have difficulty in promoting notebooks with FHD displays."

TrendForce estimates that 28% of the notebooks shipped this year worldwide will have FHD or better displays. This is a significant increase in shipment share compared with 2015. However, high prices for FHD panels will limit the penetration of FHD notebook displays. Using 15.6-inch LCD panel as an example, prices of FHD TN panels are 15~20% higher than prices of HD counterparts. Prices of 15.6-inch FHD, In-Plane Switching (IPS) panels are at least 50%, or even 100% higher in some cases, compared with prices of HD TN panels of the same size. Branded notebook vendors therefore will be hard pressed in using FHD models as replacement products for the low-end segment of the market.

If branded vendors decide to expand and promote their mid-range and high-end offerings, there is also the problem of increases in Windows license fee. Half of the branded notebooks currently available on the market carry 8GB of RAM. Based on Microsoft’s formula, a FHD display plus 8GB of RAM will lead to a large hike in Windows license fee. "Unless prices of FHD panels drop sharply or Microsoft change its license fee formula, the share of FHD models in next year’s global notebook shipments will reach just 34~35%, translating to a small increase of just 6~7 percentage points compared with the prior year," Wang noted.

Looking at the notebook OS market, Wang also pointed out that Chrome OS will continue to grow in market share during 2017. Mac OS is expected to hold 8% of the notebook OS market next year as it benefits from shipments of the latest MacBook Pro devices. Furthermore, Apple will unlikely experience notebook panel shortage in the future because the brand is a major client of panel makers. The market share of Microsoft Windows, by contrast, will keep contracting in 2017 as other branded notebook vendors face tight panel supply.

Tablets

The downward slide in tablet shipments has moderated during 2016 because Amazon’s and Huawei’s tablets have propped up the overall product sales despite the market headwinds. TrendForce estimates that global tablet shipments for 2016 will total around 154.5 million units, translating to an annual decline of 8.3%. Looking ahead to 2017, branded tablet vendors will adjust their product strategies and generate demand by releasing low-price devices. Hence, global shipments for 2017 are forecast to fall by just 5.3% annually to about 146.4 million units.

The downward slide in tablet shipments has moderated during 2016 because Amazon’s and Huawei’s tablets have propped up the overall product sales despite the market headwinds. Global market research firm TrendForce estimates that global tablet shipments for 2016 will total around 154.5 million units, translating to an annual decline of 8.3%. Looking ahead to 2017, branded tablet vendors will adjust their product strategies and generate demand by releasing low-price devices. Hence, global shipments for 2017 are forecast to fall by just 5.3% annually to about 146.4 million units.

"Most tablet brands will be more conservative in committing their resources during 2017," TrendForce notebook analyst Anita Wang pointed out. "Amazon and Huawei on the contrary have ambitions to increase their tablet shipments by many folds. The two brands are expected to expand their offerings in the near future. Additionally, Microsoft will be releasing Surface Pro 5 in the first quarter of 2017. Generally speaking, tablet shipments will drop next year but the decline will be fairly limited."

Amazon made a splash in the tablet market with price-friendly products in 2015. Since then, Amazon’s tablet shipments rose sharply for two consecutive years, and its competitors have also shifted their focus on low-price models. "To narrow Amazon’s lead in this particular segment, Apple will be introducing a more affordable 9.7-inch iPad device in the first quarter of 2017," said Wang. "While this low-price model is expected to be the main driver of iPad shipments for the entire year, whether it will be a hit with consumers remains to be seen."

Another significant trend in next year’s tablet market will be the large increase in device size. TrendForce forecasts that over 30% of tablets shipped worldwide in 2017 will be in the 10-inch and greater size segment. The 10.X-inch segment in particular will see a noticeable expansion in shipment share mainly because the leading brand Apple will also be launching a new 10.5-inch iPad device next year.

Samsung too has adjusted its product strategy and reinserted the 10.1-inch size category into its tablet offerings. Besides Apple and Samsung, other branded vendors are very active in the large-size segment as well because product margins of small-size tablets are being eroded by the intense price competition.